Private real estate prices have bottomed: We believe now is the prime entry point for investors

Private real estate prices have bottomed: We believe now is the prime entry point for investors

A reset in private real estate has occurred at a time when allocations to other asset classes are less and less attractive.

KEY TAKEAWAYS

- Prices have reset

Commercial real estate prices have bottomed, creating an entry point into an asset class that has provided steady income, capital appreciation and tax efficiency. - Limited supply meets resilient demand

Higher borrowing and construction costs have slowed new supply, demand remains resilient for most property types, and the overall backdrop is favorable for CRE. - Stocks, private credit less attractive

With the sustained period of ultra- low rates behind us, other asset classes are less attractive. Equities (listed and private) are at historically high valuations. Credit spreads are near historical lows. Private credit is showing some cracks.

This sales and advertising literature does not constitute an offer to sell nor a solicitation of an offer to buy or sell securities. An offering is made only by the prospectus. This material must be read in conjunction with the Cohen & Steers Income Opportunities REIT, Inc. prospectus in order to fully understand all of the implications and risks of the offering of securities to which the prospectus relates. A copy of the prospectus must be made available to you in connection with any offering, and is available at www.cnsreit.com. Prior to making an investment, investors should read the prospectus in its entirety, including the “Risk Factors” section therein, which contain the risks and uncertainties that we believe are material to our business, operating results, prospects and financial condition. Neither the Securities and Exchange Commission (“SEC”), the Attorney General of the State of New York nor any other state securities regulator has approved or disapproved of these securities or determined if the prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

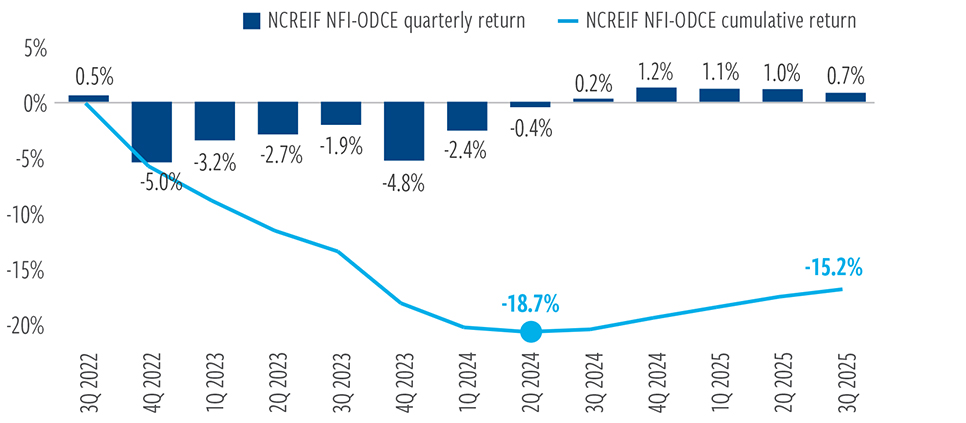

Commercial real estate prices have bottomed

Their price decline of 20% on average, peak to trough, was driven by 10 rate hikes in 2022 and 2023 that moved markets out of nearly a decade of near- zero rates and into a significantly higher cost of capital.

The resulting reset in private real estate is now an entry point for investors into an asset class that has historically provided steady income, capital appreciation and tax efficiency—at a time when other allocations are less and less attractive.

Equities (listed and private) are at historically high valuations, and listed returns are increasingly concentrated in a handful of companies benefiting from an AI-driven surge. Credit spreads are near historical lows, leaving little cushion if defaults rise or economic conditions worsen.

With the sustained period of ultra-low rates now behind us, we view those markets as having more downside than upside. Private credit, in particular, is beginning to show some cracks, in the form of concerns about stretched valuations, deteriorating underwriting standards, and elevated defaults on the back of several high-profile challenges.

Private real estate, by comparison, has repriced. U.S. private real estate, as measured by the NCREIF-ODCE index, has now posted five consecutive quarters of positive returns. This followed negative returns for seven straight quarters, dating back to the end of 2022.

Private real estate, due to its appraisal-based valuations, does not adjust to new market conditions as quickly as listed real estate, taking much longer to reprice. But once it does, it tends to build lasting momentum. The consistency of these positive returns suggests that we’re not just seeing a temporary bounce, but rather that the bottom of the market has been established.

EXHIBIT 1

Core private real estate has bottomed

Quarterly and cumulative return since peak in 3Q 2022(a)

At September 30, 2025. Source: NCREIF, Morningstar Direct, Cohen & Steers.

Past performance is no guarantee of future results. There is no guarantee that any historical trend illustrated above will be repeated in the future, and there is no way to predict precisely when such a trend will begin. The information presented above does not reflect the performance of any fund or other account managed or serviced by Cohen & Steers, and there is no guarantee that investors will experience the type of performance reflected above. (a) ODCE is represented by the NCREIF Fund Index—Open-End Diversified Core Equity Index (NFI-ODCE) – Gross Total Returns.

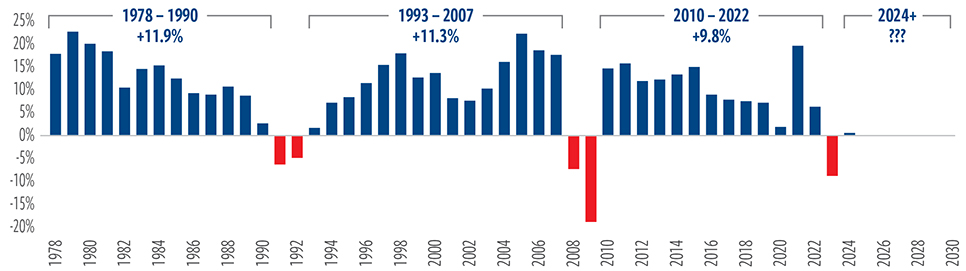

This pattern points to an emerging opportunity. There have only been three commercial real estate downturns since 1978. Each of the first two was followed by strong returns, and , while there are no guarantees, we expect similar results this time. This aligns with the pattern that once returns turn positive in commercial real estate, they remain positive, especially as the effects of the Fed easing cycle take hold.

EXHIBIT 2

Previous downturns were followed by sustained strong returns

NCREIF Property Index: Historical and average returns after negative years(a)

At December 31, 2024. Source: NCREIF, Cohen & Steers.

Data quoted represents past performance, which is no guarantee of future results. The information presented above does not reflect the performance of any fund or account managed or serviced by Cohen & Steers, and there is no guarantee that investors will experience the type of performance reflected above. There is no guarantee that any historical trend illustrated above will be repeated in the future, and there is no way to predict precisely when such a trend might begin. An investor cannot invest directly in an index, and index performance does not reflect the deductions of any fees, expenses or taxes. (a) Total returns represented by the NCREIF Property Index (NPI) gross returns. Total returns calculations are based on quarterly returns before deduction of investment management fees. The NCREIF Property Index is a quarterly, unleveraged composite total return for private commercial real estate properties held for investment purposes only; all properties in the index have been acquired, at least in part, on behalf of tax-exempt institutional investors and held in a fiduciary environment.

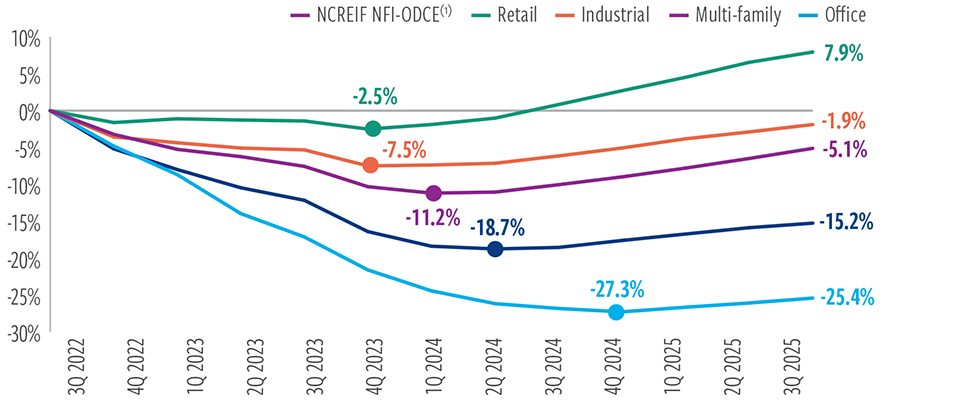

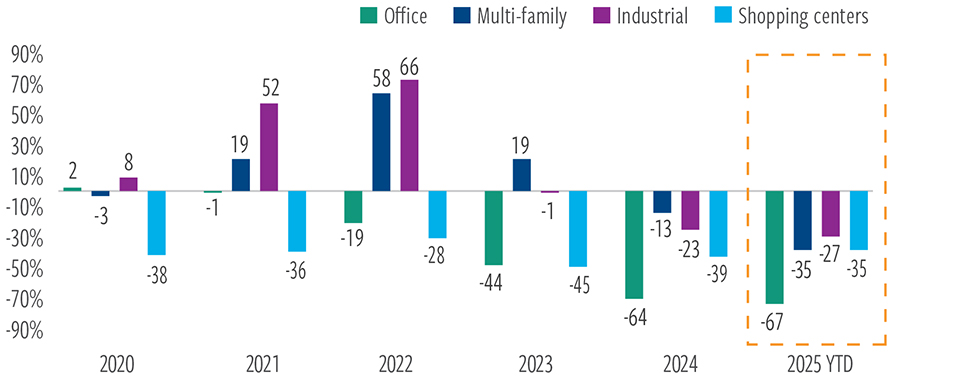

And while some sectors repriced ahead of others, evidence shows that private real estate has likely bottomed across the board. Retail hit its lows first, late in 2023. Industrial followed in late 2023, while multi-family apartments and office fell further and longer, bottoming in 1Q24 and 4Q24, respectively.

EXHIBIT 3

Values have stabilized across property sectors

Cumulative return since peak in 3Q 2022

At September 30, 2025. Source: NCREIF, Morningstar Direct, Cohen & Steers.

Past performance is no guarantee of future results. There is no guarantee that any historical trend illustrated above will be repeated in the future, and there is no way to predict precisely when such a trend will begin. The information presented above does not reflect the performance of any fund or other account managed or serviced by Cohen & Steers, and there is no guarantee that investors will experience the type of performance reflected above. (a) ODCE is represented by the NCREIF Fund Index—Open-End Diversified Core Equity Index (NFI-ODCE) – Gross Total Returns.

This doesn’t mean that the tide will rise or rise at the same rate for all property types from here. We believe retail is situated to reaccelerate from current levels, though not blindly across the board. Property selection will matter, as property types, business models, locations and valuations vary.

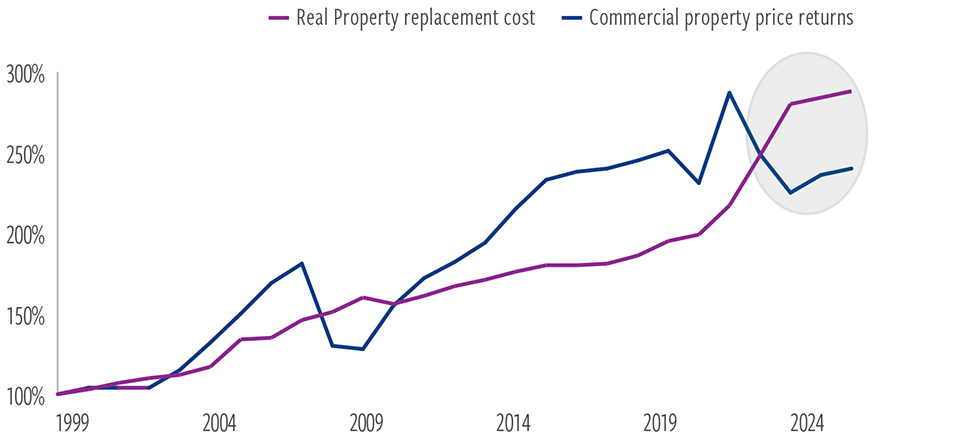

Still, we see opportunities driven by supply and demand dynamics that favor expected returns for commercial real estate. While some property types have been more constrained than others, economic uncertainty, higher borrowing costs, and inflationary pressures on building costs (notably, materials and wages) have slowed new construction.

Inflation on materials and labor, combined with higher borrowing costs, mean that it simply costs more to build than to buy, and this disincentive to build will enable accelerating rent growth for existing properties. Mortenson’s Construction Cost Index shows that nonresidential construction costs have climbed more than 40% since 2020 and are up nearly 7% in just the last 12 months.

The result is that new supply isn’t coming any time soon. Given that real estate prices tend to track replacement costs, we view the current data as a strong buy signal.

EXHIBIT 4

It is now cheaper to buy than build

Commercial property price return vs. real property replacement cost (index=100)(a)

At September 30, 2025. Source: Zurich, Green Street, Cohen & Steers.

Past performance is no guarantee of future results. There is no guarantee that any historical trend illustrated above will be repeated in the future, and there is no way to predict precisely when such a trend will begin. The information presented above does not reflect the performance of any fund or other account managed or serviced by Cohen & Steers, and there is no guarantee that investors will experience the type of performance reflected above. (a) Real property replacement cost represented by Zurich Replacement Value Cost Trends, January 2025. The cost trends are published to assist in maintaining proper levels of insurable replacement costs for commercial and industrial properties. Commercial property price returns are represented by Green Street’s Commercial Property Price Index (CPPI). Green Street’s CPPI is a proprietary time series of U.S. commercial property values that captures the prices at which commercial real estate transactions are currently being negotiated and contracted.

In fact, U.S. construction starts for every major property type were below their 10-year average in 2024 and 2025 (year to date at November 25).

EXHIBIT 5

Tight supply should drive “rent growth”

U.S. construction starts vs. 10-year average by sector (% of inventory)

At November 25, 2025. Source: CoStar, Cohen & Steers.

Data quoted represents past performance, which is no guarantee of future results.

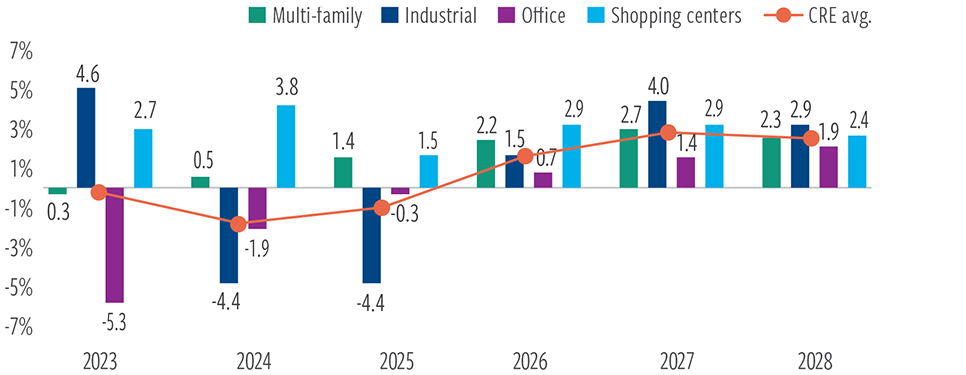

We expect that lower supply and resilient demand will drive accelerating fundamentals and property values for commercial real estate. This is emerging, we believe, in a recent uptick in transaction volumes.

EXHIBIT 6

Accelerating fundamentals

Growth in market revenue per available foot (measured by market rents and occupancy rates)(a)

At September 30, 2025. Source: NCREIF, Cohen & Steers.

Data quoted represents past performance, which is no guarantee of future results. The information presented above does not represent the performance of any fund or other account managed or serviced by Cohen & Steers, and there is no guarantee that investors will experience the type of performance listed above. There is no guarantee that any historical trend illustrated above will be repeated in the future, and there is no way to predict precisely when such a trend might begin. There is no guarantee that any market forecast set forth in this presentation will be realized. (a) Market revenue per available foot (M-RevPAF) is a measure of the health of a market (or sector) that combines two key operating metrics (effective market rents and occupancy) into a single value.

Comparing real estate to equities and credit

The case for private real estate looks particularly compelling when compared with other asset allocations.

First, equity markets (both listed and private) are at historically high valuations and are, we believe, unlikely to provide the double-digit returns they have averaged over what’s now been more than a decade-long supercycle.

The equity market’s winners are also increasingly concentrated on the potential for artificial intelligence capital investment and returns. We believe investors should consider allocations away from such concentrated risk at such elevated valuations.

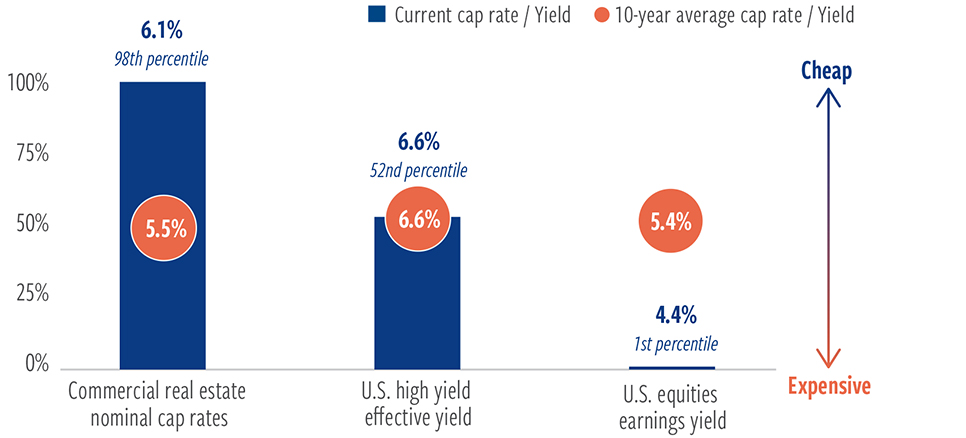

EXHIBIT 7

Valuations are cheap versus other risk assets

Commercial real estate, equities and high yield valuation percentiles(a)

At October 31, 2025. Source: Bloomberg, Green Street, Cohen & Steers.

Data quoted represents past performance, which is no guarantee of future results. There is no guarantee that any historical trend illustrated above will be repeated in the future, and there is no way to predict precisely when such a trend will begin. The information presented above does not reflect the performance of any fund or other account managed or serviced by Cohen & Steers, and there is no guarantee that investors will experience the type of performance reflected above. (a) Commercial real estate nominal cap rates are represented by Green Street’s nominal cap rates, which are the expected unleveraged first-year yield a property buyer expects to realize on their investment. Like bond yields, nominal cap rates move inversely with property values. U.S. high yield effective yield is represented by the ICE BofA U.S. High Yield Index, which tracks the performance of U.S. dollar-denominated below-investment-grade rated corporate debt publicly issued in the U.S. domestic market. U.S. equities earnings yield is represented by the S&P 500 Index, which measures the performance of approximately 500 of the largest publicly traded companies in the United States.

Meanwhile, there are several reasons to believe private markets will struggle to repeat their extraordinary returns and (likely mischaracterized) low volatility of the past decade.

As mentioned earlier, the opportunity for private assets to lever investments at ultra-low and stable interest rates has largely vanished. At the same time, flows into private equity and private credit have surged, which we believe will challenge future returns.

Private credit’s explosive growth to $2 trillion AUM—ten times its 2009 size— has intensified competition among lenders. More lenders chasing borrowers creates concerns about lower underwriting standards. This concentration of capital pursuing the same deals suggests private credit returns may gradually converge toward traditional corporate bond market levels, challenging the sector’s “all-weather” reputation despite its attractive yield component.

In private equity, exits (as measured by transaction value, according to S&P Global) have fallen by nearly half their total since 2021, the last full year before rate hikes hit. The result is a backlog of investments that ties up capital, extends holding periods, and increases valuation risk, ultimately diluting potential returns for investors.

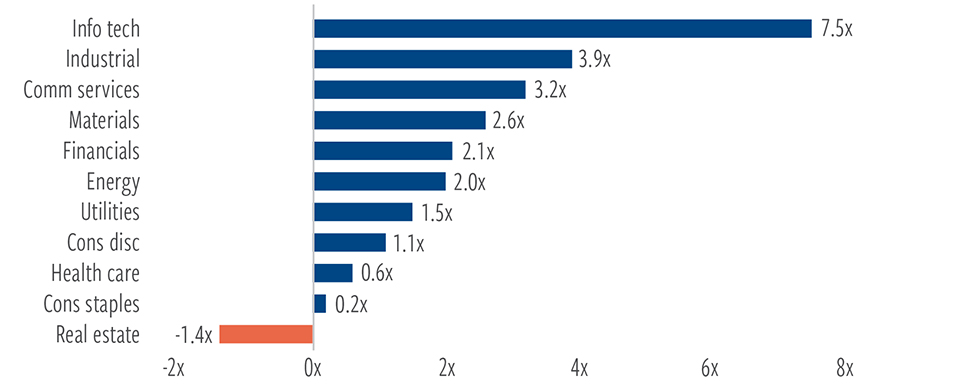

By comparison, real estate, which has already repriced for the next phase of the cycle, appears increasingly attractive. One notable measure: Real estate is now the only sector of the S&P 500 trading below its five-year average earnings multiple.

Considering that REITs provide a real-time indicator of value opportunity currently available in real estate, we believe this portends well for private real estate returns as well.

EXHIBIT 8

Real estate is the only GICS sector trading below 5-year average earnings

GICS sector current earnings multiples vs. 5-year average(a)

At October 31, 2025. Source: Bloomberg, Cohen & Steers.

Data quoted represents past performance, which is no guarantee of future results. There is no guarantee that any historical trend illustrated above will be repeated in the future, and there is no way to predict precisely when such a trend will begin. The information presented above does not reflect the performance of any fund or other account managed or serviced by Cohen & Steers, and there is no guarantee that investors will experience the type of performance reflected above. (a) Represented by the S&P 500 Index, which measures the performance of approximately 500 of the largest publicly traded companies in the United States.

The long-term case for private real estate

The reset in prices, supply/demand dynamics, and the relatively favorable profile of commercial real estate (compared with alternative allocations) are compelling. And that creates an unusual opportunity to access the long- term benefits of private real estate, in our view.

Understandably, perhaps, commercial real estate has been out of favor. According to the 2025 Real Estate Allocations Monitor, institutional investors reduced their target allocations to real estate for the first time in four years, albeit by just 10 basis points. But those same investors are below their target allocations by 90 basis points.

By comparison, individual investors often completely overlook real estate— the third-largest asset class in the world, behind stocks and bonds—when diversifying their portfolios beyond the traditional 60/40 mix.

Institutional investors, which have access to extensive research and professional analysts (and often decades of experience), as well as access to more vehicles and the ability to invest in private real estate, allocate 3.5 times as much of their capital to real estate than individual investors, on average.

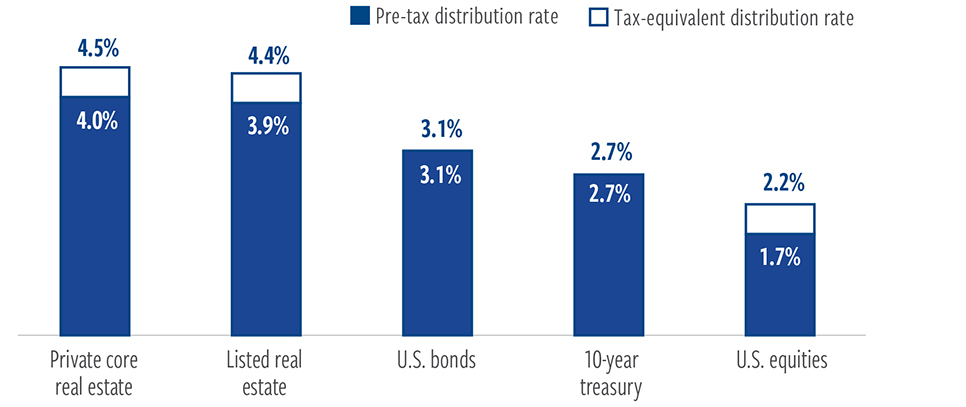

We believe private real estate, especially when combined with listed real estate allocations, can and should help investors diversify, create more resilient portfolios, and improve Sharpe ratios given more attractive valuations and greater inflation sensitivity. Private real estate, in particular, presents investors with the opportunity for high tax-efficient yields, compared with other asset classes.

EXHIBIT 9

Reliable source of income with potential tax advantages

Average 10-year distribution rates(a)

At December 31, 2025. Source: Cohen & Steers, Morningstar.

Data quoted represents past performance, which is no guarantee of future results. Private core real estate: NCREIF Fund Index –Open End Diversified Core Equity (NFI-ODCE); Listed real estate: FTSE Nareit All Equity REITs Index; U.S. equities: S&P 500 Index; U.S. bonds: Barclays U.S. Aggregate Bond Index; 10-year treasury: Barclays U.S. Treasury 5-7 Yr Index. (a) Average distribution rate calculated on a quarterly frequency for the trailing 10-year period ending December 31, 2022. After-tax calculation assumes taxation at the highest marginal tax rate for each security income type. Assumes all real estate securities yield is eligible for the 20% Qualified Business Income deduction. Does not include the Medicare surcharge of 3.8% nor state and local taxes.

Real estate also has historically had low correlations to traditional asset classes, which matters at a time when investors are seeking more diversification, and given that stock and bond valuations are historically high.

Finally, too often, high-net-worth investors believe owning property covers their real estate allocations, but directly investing in real estate comes at a cost of illiquidity, high transaction expense (up to 5% during buying and selling), time-consuming management of a property (or the costs of employing a property manager), and large upfront costs.

Investing in a private real estate fund offers diversification, tax benefits, greater liquidity than direct investing, low-cost entry, and potential regular income and returns over time. The bottoming of private real estate prices gives investors a compelling entry point to potentially benefit from those attributes.

Non-traded REITs: A new era of liquidity, transparency and lower fees

Three main drivers lie at the heart of growing investor interest in private real estate: 1) investor calls to diversify their portfolios with alternatives (such as private real estate); 2) a continued and growing demand for attractive total returns, particularly through current income; and 3) a democratization of private real estate investing through new regulated funds.

One fund structure has gained particular traction in recent years: non-traded REITs (NTRs). A new generation of NTRs, which were first launched in 2016, has improved investor confidence in the funds. By comparison, the earlier generation of NTRs drew significant scrutiny.

We believe the differences between the earlier vehicles (known as “life cycle” REITs) and the newer vehicles (known as “net asset value,” or NAV, REITs) warrant clarification and comparison.

- Lower costs: Gone are the high upfront commissions and opaque fees. Newer NTRs feature share classes with no selling commissions and capped service fees.

- Improved liquidity: Monthly repurchase programs and perpetual, open-ended structures provide investors with access to capital while protecting portfolios from forced sales.

- Enhanced transparency and oversight: Independent appraisals and monthly NAV reporting improve transparency. Management by global firms with multiple layers of governance—including independent auditors as well as risk, trading and valuation committees—offers greater oversight.

- Tax simplicity: For tax purposes, NTRs are structured as corporations or trusts, not as partnerships. This means they report shareholder distributions using Form 1099-DIV, not Schedule K-1. A 1099-DIV is straightforward; it summarizes dividends and capital gains, making tax filing easier. In contrast, a K-1 includes detailed allocations of income, deductions and credits, often requiring professional help and delaying tax filings.

Sign up to get CNSREIT alerts delivered to your inbox

ABOUT THE AUTHORS

FURTHER READING

View all insights

The tax advantages of real estate investing

June 2026 | 5 mins

REITs have a history of attractive distributions before and after taxes.

As private real estate bottoms, an opportunity emerges in retail

November 2025 | mins

Strong demand is colliding with extremely low supply for open-air, necessity driven shopping centers.

The Retail Apocalypse is over; The Retail Renaissance has arrived

March 2025 | 6 mins

Reports of the death of the store were greatly exaggerated.

Important considerations

Cohen & Steers Income Opportunities REIT, Inc. (“CNSREIT”) is a newly organized corporation formed to invest primarily in high quality, income-focused, stabilized assets within the United States. This investment involves a high degree of risk. You should purchase these securities only if you can afford the complete loss of your investment. You should read the prospectus (https://www.cnsreit.com/prospectus) carefully for a description of the risks associated with an investment in CNSREIT. These risks include, but are not limited to, the following:

- We have held our current investments for a limited time and you will not have the opportunity to evaluate our future investments before we make them, which makes investment in our common stock more speculative.

- Because this is a “blind pool” offering, you will not have the opportunity to evaluate our future investments before we make them.

- There is no public trading market for shares of our common stock and repurchase of shares by us will likely be the only way to dispose of your shares. We are not obligated to repurchase any shares and may choose to repurchase only some, or even none, of the shares that have been requested to be repurchased in any particular month in our sole discretion. In addition, repurchases will be subject to available liquidity and other significant restrictions. Further, our board of directors may make exceptions to modify or suspend our share repurchase plan. As a result, our shares should be considered as having only limited liquidity and at times may be illiquid.

- Distributions are not guaranteed and may be funded from sources other than cash flow from operations, including, without limitation, the sale of or repayments under our assets, borrowings, return of capital or offering proceeds, and we have no limits on the amounts we may pay from such sources.

- The purchase and repurchase price for shares of our common stock are generally be based on our prior month’s net asset value (“NAV”) and are not based on any public trading market. While there will be independent valuations of our properties from time to time, the valuation of properties is inherently subjective and our NAV may not accurately reflect the actual price at which our properties could be liquidated on any given day.

- We are dependent on the Cohen & Steers Capital Management, Inc. (the “Adviser”) to conduct our operations. The Adviser will face conflicts of interest as a result of, among other things, the allocation of investment opportunities among us and other Cohen & Steers Accounts (as defined in CNSREIT’s prospectus), the allocation of time of its investment professionals and the fees that we will pay to the Adviser.

- There are limits on the ownership and transferability of our shares.

- This is a “best efforts” offering. If we are not able to raise a substantial amount of capital in the near term, our ability to achieve our investment objectives could be adversely affected.

- If we fail to qualify as a REIT and no relief provisions apply, our NAV and cash available for distribution to our stockholders could materially decrease.

- While our investment strategy is to invest in income-focused stabilized private real estate with a focus on providing current income to investors, there is no guarantee that we will achieve this strategy and an investment in us is not an investment in a fixed income instrument.

- The use of leverage involves a high degree of financial risk and will increase the exposure of the investments to adverse economic factors.

- Investing in commercial and other private real estate assets involves certain risks, including but not limited to: tenants’ inability to pay rent; increases in interest rates and lack of availability of financing; tenant turnover and vacancies; and changes in supply of or demand for similar properties in a given market.

- Substantial risks are involved in investing in real estate and real estate-related securities more generally. An unstable geopolitical climate and central bank policies could have a material adverse effect on general economic conditions, market conditions and liquidity. Additionally, a serious pandemic or natural disaster could severely disrupt global, national and/or regional economies, as experienced most recently after the March 2020 outbreak of COVID-19. Renewed outbreaks or the outbreak of new epidemics could result in health or other government authorities requiring the closure of offices or other businesses, including office buildings, retail stores and other commercial venues and could also result in a general economic decline.

We do not own the Cohen & Steers name, but we are permitted to use it as a part of our corporate name pursuant to a license agreement with an affiliate of Cohen & Steers.

This material must be read in conjunction with CNSREIT’s prospectus in order to fully understand all the implications and risks of an investment in CNSREIT. Please refer to the prospectus for more information regarding state suitability standards and consult a financial professional for share class availability and appropriateness.

Neither the Securities and Exchange Commission (“SEC”), the Attorney General of the State of New York nor any other state securities regulator has approved or disapproved of these securities or determined if the prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

THIS MATERIAL IS NEITHER AN OFFER TO SELL NOR A SOLICITATION OF AN OFFER TO BUY SECURITIES. An offering is made only by the prospectus, which must be made available to you in connection with this offering and is available at www.CNSREIT.com/prospectus. Prior to making an investment, investors should read the prospectus in its entirety, including the “Risk Factors” section therein, which contain the risks and uncertainties that we believe are material to our business, operating results, prospects and financial condition.

Cohen & Steers Securities, LLC (“CSS”) is a broker-dealer whose purpose is to distribute Cohen & Steers managed or affiliated products. CSS provides services to affiliates, not to investors in its funds, strategies or other products. CSS will not make any recommendation regarding, and will not monitor, any investment. As such, when CSS presents an investment strategy or product to an investor or a prospective investor, CSS does not collect the information necessary to determine-and CSS does not engage in a determination regarding-whether an investment in the strategy or product is in the best interests of, or is suitable for, the investor. You should exercise your own judgment and/or consult with your own investment professional to determine whether it is advisable for you to invest in any Cohen & Steers strategy or product. CSS will not provide the kinds of financial services that you might expect from another financial intermediary, such as overseeing any brokerage or similar account. For financial advice relating to an investment in any Cohen & Steers strategy or product, contact your own financial professional.

CNSREIT is distributed by Cohen & Steers Securities, LLC.