The tax advantages of real estate investing

The tax advantages of real estate investing

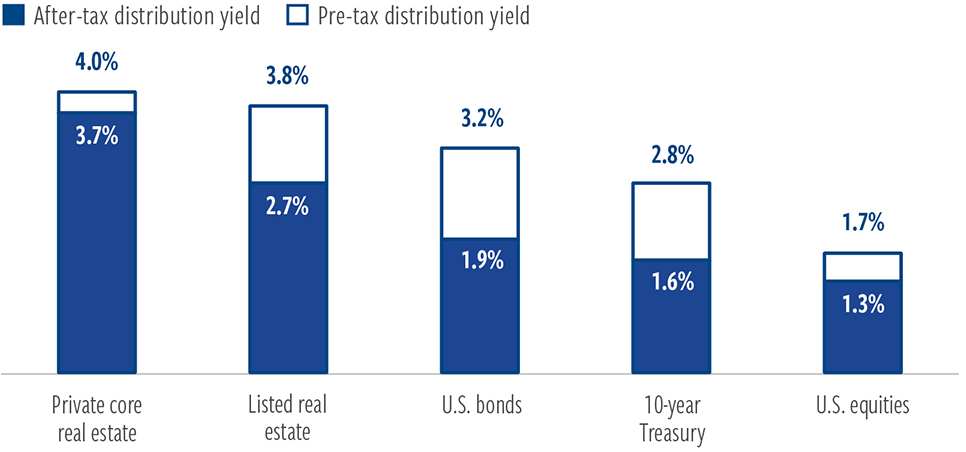

REITs have a history of attractive distributions before and after taxes.

Investment solutions with inherent tax efficiencies may help investors diversify sources of income and potentially keep more of what they earn. REITs, in particular, have a history of attractive distributions before and after taxes.

To start, REITs benefit from a 20% tax deduction on ordinary income, which can reduce the tax rate on ordinary income distributions to investors.

Due to depreciation deductions, REITs also have the ability to characterize a portion of distributions received as return of capital (ROC). Depreciation refers to a non-cash tax deduction that allows investors to expense a portion of a property’s value over its useful life, reducing taxable income without impacting cash flow. ROC distributions are tax deferred until redemption, at which time they are characterized as capital gains.

Gains from the sale of private and listed real estate held longer than one year are typically taxed as long-term capital gains, which are subject to lower federal tax rates than ordinary income.

The result: Listed and private real estate offer reliable sources of income with potentially higher tax advantages over traditional bonds and stocks. Over the last 10 years, private core real estate and listed real estate have delivered 5.87% and 4.29% tax-equivalent distribution rates, respectively. That compares with 3.1% for U.S. bonds and just 2.2% for U.S. equities.

Reliable source of income with potential tax advantages

Average 10-year distribution rates(1)

At March 31, 2026. Source: Cohen & Steers, Morningstar.

Data quoted represents past performance, which is no guarantee of future results.

Qualified business income (QBI)

REIT distributions receive a 20% deduction on ordinary income, reducing the tax rate from

37% to 29.6% for top earners.(2)

Long-term capital gain

Gains are taxed at a 20% rate for top earners.

Return of capital (ROC)

A portion of dividends as return of capital (ROC). ROC distributions are tax deferred until redemption, at which time they are characterized as capital gains.(3)

Depreciation deduction

REITs can deduct depreciation, which reduces taxable income.

Sign up to get CNSREIT alerts delivered to your inbox

FURTHER READING

View all insights

Private real estate prices have bottomed: We believe now is the prime entry point for investors

February 2026 | 31 mins

A reset in private real estate has occurred at a time when allocations to other asset classes are less and less attractive.

As private real estate bottoms, an opportunity emerges in retail

November 2025 | mins

Strong demand is colliding with extremely low supply for open-air, necessity driven shopping centers.

The Retail Apocalypse is over; The Retail Renaissance has arrived

March 2025 | 6 mins

Reports of the death of the store were greatly exaggerated.

Index definitions and important disclosures

Data quoted represents past performance, which is no guarantee of future results. There is no guarantee that any historical trend illustrated above will be repeated in the future, and there is no way to predict precisely when such a trend will begin. The information presented above does not represent the performance of any fund or other account managed or serviced by Cohen & Steers, and there is no guarantee that investors will experience the type of performance listed above.

Performance represented by the following: Private Core Real Estate NCREIF Fund Index –Open End Diversified Core Equity (NFI-ODCE). Listed Real Estate: FTSE Nareit All Equity REITs Index; U.S. Equities: S&P 500 Index; U.S. Bonds: Barclays US Aggregate Bond Index; 10-Year Treasury: Gov’t 10 Yr Index (1) Average distribution rate calculated on a monthly frequency for the trailing 10-year period ending March 31, 2026. Private real estate rate is as of December 31, 2025. After tax calculations assumes taxation at the highest marginal tax rate for each security income type. Assumes all real estate securities yield is eligible for the 20% Qualified Business Income deduction. Includes the Medicare surcharge of 3.8%. Does not include state and local taxes. (2) The description of tax consequences contained herein limited to the U.S. federal income tax consequences to a taxable U.S. person. (3) Return of capital (ROC) distributions are distributions in excess of current or accumulated earnings and profits. Such distributions are not taxable to an investor to the extent they do not exceed the investor’s tax basis in its shares. Rather, the ROC reduces an investor’s tax basis in the year the distribution is received and generally defers taxes on that portion of the distribution until the investor’s stock is sold via redemption. To the extent that a ROC exceeds an investor’s tax basis, it generally will be taxable as a capital gain. Such gain will be long-term capital gain if the investor has held its shares for than one year.

This material represents an assessment of the market environment at a specific point in time and should not be relied upon as investment advice, does not constitute a recommendation to buy or sell a security or other investment and is not intended to predict or depict performance of any investment. This material is not being provided in a fiduciary capacity and is not intended to recommend any investment policy or investment strategy or take into account the specific objectives or circumstances of any investor. We consider the information in this presentation to be accurate, but we do not represent that it is complete or should be relied upon as the sole source of appropriateness for investment. Please consult with your investment, tax or legal professional regarding your individual circumstances prior to investing. An investor cannot invest directly in an index and index performance does not reflect the deduction of any fees, expenses or taxes. Index comparisons have limitations as volatility and other characteristics may differ from a particular investment.

Risks of Investing in Real Estate Securities

Risks of investing in real estate securities are similar to those associated with direct investments in real estate, including falling property values due to increasing vacancies or declining rents resulting from economic, legal, political or technological developments, lack of liquidity, limited diversification and sensitivity to certain economic factors such as interest rate changes and market recessions. Foreign securities involve special risks, including currency fluctuations, lower liquidity, political and economic uncertainties, and differences in accounting standards. Some international securities may represent small- and medium-sized companies, which may be more susceptible to price volatility and less liquidity than larger companies.

No representation or warranty is made as to the efficacy of any particular strategy or fund or the actual returns that may be achieved.

Risks of Investing in Private Real Estate

Private real estate investments are illiquid and susceptible to economic slowdowns or recessions and industry cycles, which could lead to financial losses and a decrease in revenues, net income and assets. Lack of liquidity in the private real estate market makes valuing underlying assets difficult. Appraisal values may vary substantially from a price at which an investment in real estate may actually be sold.

Cohen & Steers Capital Management, Inc. (Cohen & Steers) is a U.S. registered investment advisory firm that provides investment management services to corporate retirement, public and union retirement plans, endowments, foundations and mutual funds. Cohen & Steers U.S. registered open-end funds are distributed by Cohen & Steers Securities, LLC and are only available to U.S. residents. Cohen & Steers Asia Limited is authorized and regulated by the Securities and Futures Commission of Hong Kong (ALZ367). Cohen & Steers Japan Limited is a registered financial instruments operator (investment advisory and agency business and discretionary investment management business with the Financial Services Agency of Japan and the Kanto Local Finance Bureau No. 3157) and is a member of the Japan Investment Advisers Association. Cohen & Steers UK Limited is authorized and regulated by the Financial Conduct Authority (FRN458459). Cohen & Steers Ireland Limited is regulated by the Central Bank of Ireland (No. C188319). Cohen & Steers Singapore Limited is a private company limited by shares in the Republic of Singapore.